Manage Your Debt - Let's Explore Your Options

GET STARTED NOWAuto Loan: Bank or Dealership

If you are thinking about buying a car, you have probably wondered whether it is better to use dealer financing or finance through a bank or credit union. With dealer-arranged financing, the dealer collects information from you and forwards that information to one or more prospective auto lenders. Alternatively, with bank or other lender financing, you go directly to a bank, credit union, or finance company and apply for a loan. We refer to this type of loan as a “direct loan.”

Why Choose a Direct Auto Loan?

If you apply for a direct loan through a bank or credit union, they may preapprove you for a loan. This means they will quote you an interest rate, loan term (number of months), and a maximum loan amount. These figures will be based on several factors such as your credit score, terms of the transaction, type of vehicle and your debt-to-income ratio. You can then take the quote or a conditional commitment letter to the dealership.

A big benefit of being preapproved is that the only item to negotiate with the dealer is the price of the vehicle and any other extra’s you want to include in the purchase.

How Dealer-Arranged Financing Works

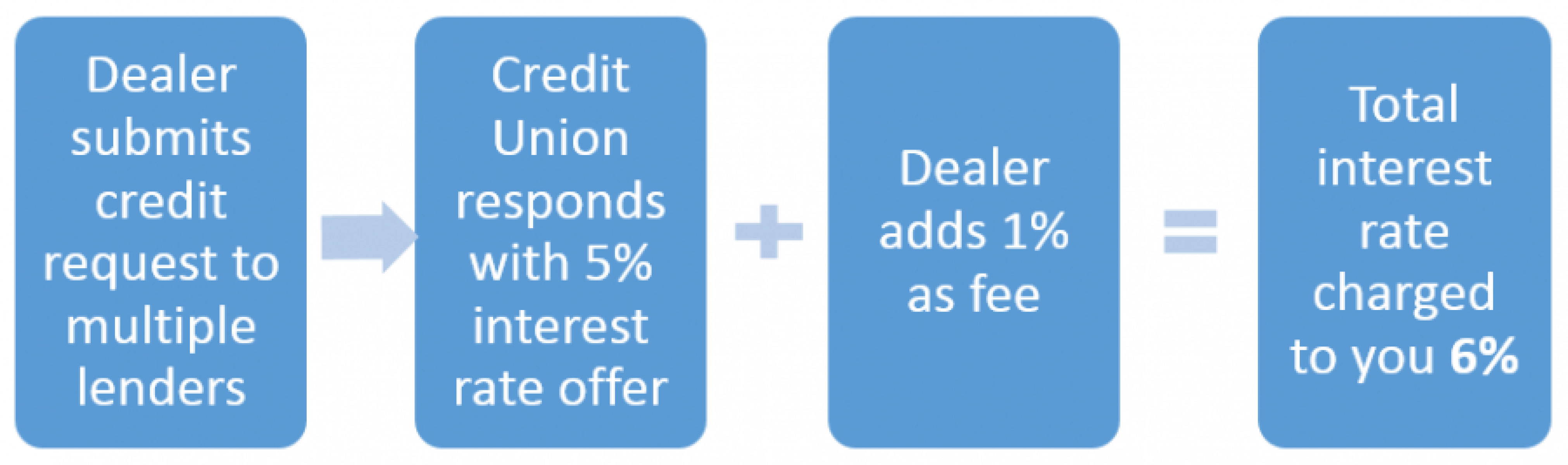

In dealer-arranged financing the dealer collects information from you and forwards that information to one or more potential auto lenders. If the lender(s) chooses to finance your loan, they may authorize or quote an interest rate to the dealer to finance the loan, referred to as the “buy rate.” The interest rate that you negotiate with the dealer may be higher than the “buy rate” because it may include an amount that compensates the dealer for handling the financing.

As an example, the dealership sends your credit request to several different lenders (banks, credit unions, etc.) with whom they have a relationship. A credit union responds with a buy rate of 5%. The dealer then states the interest rate as 6% to you. The additional 1% goes to the dealer to pay for their time in putting together the loan.

You may be able to negotiate the interest rate quoted to you by the dealer. Ask or negotiate for a loan with better terms. Be sure to compare the financing offered through the dealership with the rate and terms of any pre-approval you received from a bank, credit union, or other lender. Choose the option that best fits your budget.

Final Word in Dealer Financing

Some types of dealerships finance auto loans “in-house” to borrowers with no credit or poor credit. At “Buy Here Pay Here” dealerships, you might see signs with messages like “No Credit, No Problem!” The interest rate on loans from these dealerships can be much higher than loans from a bank, credit union, or other type of lender. Consider whether the cost of the loan outweighs the benefit of buying the vehicle. Even if you have poor or no credit, it may be worth it to see if there is a bank, credit union, or another dealer that is willing to make a loan to you. Another feature of this type of dealership is that your monthly payment is made to the dealership rather than the bank or credit union. Some Buy Here Pay Here Dealerships, and some other lenders that lend to people with no credit or poor credit, put devices in their vehicles that help them repossess or disable the vehicle if you miss a payment.

Buying a car is a big decision, especially when it comes to your money. Be sure to examine the terms (payment, length and interest rate) of all offers. If you are wondering how a payment may fit in your budget, contact a credit counselor. They can review your income and expenses with you and may be able to help you reduce debts in order to better afford a vehicle.

Compiled in part with information from the Consumer Financial Protection Bureau.

Published Mar 19, 2018.