Manage Your Debt - Let's Explore Your Options

GET STARTED NOWAlternative Payment Arrangements for Unexpected Expenses

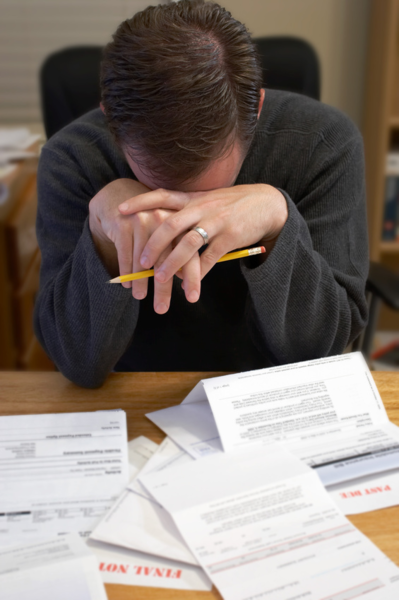

Someday you might be forced to confront a bill there is no way you could pay right away. It’s often, in situations like this, that consumers immediately resort to using credit cards. It might be for a necessary expense. And that, you tell yourself, is exactly why you should have a credit card or two in the first place, to handle emergencies.

You might be able to save yourself a lot of money, though, before you resort to breaking out the plastic. Ask the people providing you the service if they will accept payments.

Take an unexpected medical expense. It’s easy to see why you might not think to ask a doctor or a hospital if you can make payments. Health care facilities don’t look like financial institutions and their willingness to take payments over time is certainly not something they often advertise up front. But in most cases they do, often for no interest at all.

Of course, you would have more time to pay an $800 medical bill if you use a credit card to pay it off. But the average credit card interest rate is in the neighborhood of 15 percent. At that rate it would take you 70 months and an additional $365 in interest to pay that credit card off. Your credit card interest rate may be even higher.

On the other hand, a health care provider might want you to pay off that $800 bill in four or five months. While that can seriously affect your budget temporarily, it’s good to get the debt behind you.

Another place to ask for payments is the government if you owe on taxes. You will likely pay interest on that debt for as long as you are making payments, but it’s unlikely to be more than what you would pay on a credit card.

This might also seem strange to you, but if you get an expensive traffic ticket sometimes your local government will allow you to make payments. They often won’t charge interest either. Again, you will probably have to pay it off faster than you would with a credit card, but it will be worth it to not have it linger as a debt burden. Another hint about traffic fines, judges will often reduce your fine if you ask in the right way.

We advise you to incur as little debt as possible for attending college, but if you need to borrow you are far better off getting a federally backed student loan than using a credit card. Again, the interest is lower and the payments are deferred as long as you are still in school. Some colleges offer short-term payment programs, too.

There may be occasions when you will be unable to avoid using credit cards to pay for services or products you need. And in some cases if you are buying something you must borrow to pay for, your credit card will provide a better deal than a retailer would. The best advice you can take, though, is to ask what options are available, wherever you are.

For more information about the best ways to address potential debts, contact the credit counselors at American Financial Solutions. There you will get useful information about ways to approach those times when you know you will have to incur debt and make payments over time.

Published Apr 2, 2014.